Traffic to and from the Middle East continues to defy the global trend with RPKs up almost 10% in May. Etihad launched Abu Dhabi-Istanbul services on 1 June.

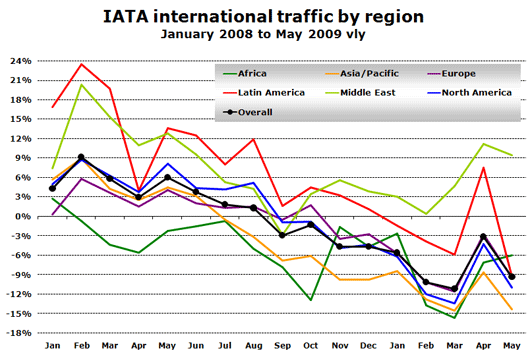

The latest figures published by IATA show that its 230 member airlines reported an overall decline of 9.3% in international RPKs (revenue passenger kilometres) during May. Aprils figures showed some improvement with international RPKs down just over 3% but this can be attributed to the re-timing of Easter this year.

Source: IATA

Source: IATA

Only traffic to and from the Middle East continues to defy the global trend with RPKs up almost 10% in May. Across all regions capacity (ASKs - available seat kilometres) fell less quickly than demand (RPKs). While RPKs were down 9.3% capacity was down just 5% as the average load factor fell by 3.2 points from 74.5% a year ago to 71.2%. IATA acknowledges that while international RPKs in Europe for IATA member airlines fell by 9.4% in May, low cost airlines gained market share as their RPKs grew by 2.1%.

Premium traffic falls 22% in April

According to IATA premium traffic (people travelling on first or business class tickets) fell by 22.0% in April. While Easter will have had a (negative) impact on the demand for business travel in April this is still an alarming statistic for legacy airlines. Combined with IATAs estimate that average premium fares were down by 22% in March, then revenue from business travel in April may have been down as much as 40%. No wonder airlines such as British Airways feel the need to take drastic action regarding costs as they adjust to the new reality of their business model.

The latest figures published by IATA show that its 230 member airlines reported an overall decline of 9.3% in international RPKs (revenue passenger kilometres) during May. Aprils figures showed some improvement with international RPKs down just over 3% but this can be attributed to the re-timing of Easter this year.

Only traffic to and from the Middle East continues to defy the global trend with RPKs up almost 10% in May. Across all regions capacity (ASKs - available seat kilometres) fell less quickly than demand (RPKs). While RPKs were down 9.3% capacity was down just 5% as the average load factor fell by 3.2 points from 74.5% a year ago to 71.2%. IATA acknowledges that while international RPKs in Europe for IATA member airlines fell by 9.4% in May, low cost airlines gained market share as their RPKs grew by 2.1%.

Premium traffic falls 22% in April

According to IATA premium traffic (people travelling on first or business class tickets) fell by 22.0% in April. While Easter will have had a (negative) impact on the demand for business travel in April this is still an alarming statistic for legacy airlines. Combined with IATAs estimate that average premium fares were down by 22% in March, then revenue from business travel in April may have been down as much as 40%. No wonder airlines such as British Airways feel the need to take drastic action regarding costs as they adjust to the new reality of their business model.